1

Please refer to important disclosures at the end of this report

1

1

Leading security services player offers secure returns

Incorporated in 1985, Security and Intelligence Services (India) Limited (SIS)

provides private security and facility management services in India and Australia.

They offer cash logistics & security services, including manned guarding and

electronic security; and facility management services, such as mechanized

cleaning, and pest & termite control services.

Leadership position in all the segments: In terms of revenue SIS is the 2nd largest

security services provider in the cash logistic segment in India, and it is growing at

a rapid pace. Company’s revenue from security services business in India grew at

29.7% CAGR (FY2013-17). Further, SIS acquired Dusters, the fourth largest

facility management service provider in India (in terms of revenues), as of March

31, 2016, according to Frost & Sullivan. SIS’s brand is well-recognized for

providing quality services in India and Australia and the management believes

that strong brand positioning and strategic focus on such business has contributed

to sustained increase in business over the years.

Variety of services coupled with diverse customer base: SIS’s customer segments

range across a variety of sectors including banking and financial services, IT/ ITeS

& telecom, automobile, steel & heavy industries, governmental undertakings,

hospitality & real estate, utilities, educational institutions, healthcare, consumer

goods, engineering and construction, which therefore, reduces vulnerabilities to

economic cycles and dependence on any particular set of customers. SIS’s diverse

portfolio of services comprises of security services, cash logistics services,

electronic security & home alarm monitoring and response, as well as facility

management services. SIS’s multiple service offerings allow to derive operational

efficiencies by centralizing key functions.

Inorganic growth through strategic acquisitions: SIS acquired 78.72% equity in

Dusters Total Solutions Services Pvt. Ltd (4

th

largest) with an agreement to increase

its shareholding to 100% over the next three years. SIS, through its 100%

subsidiary, SIS Australia Group Pty Ltd., acquired 51% equity in Andwills Pty Ltd.,

which contributes ~60% of total revenues. While continuing to maintain organic

growth momentum, SIS intends to explore inorganic expansion as well, leveraging

on the experience the company has gained through its previous acquisitions.

Outlook and Valuation: At the upper price band of `815, issue is offered at 61x

FY17EPS (Pre issue marketcap), which is at ~36% discount to Quess Corp (96x

FY2017EPS). Moreover, SIS has better ROE (16.4%) compared to Quess Corp

(13.6%). Furthermore, at 10.3xP/BV, 26.2xEV/EBITDA, SIS’s valuation looks

attractive compared to Quess Corp’s valuation of 13.1xP/BV, 50.4xEV/EBITDA.

Hence, we recommend SUBSCRIBE rating on the issue.

Key Financials

Y/E March (` cr)

FY2013

FY2014

FY2015

FY2016

FY2017

Net Sales

2644

3098

3551

3836

4567

% chg

17.2

14.6

8.0

19.1

Net Profit

57

69

63

76

91

% chg

20.1

-8.7

20.8

20.5

OPM (%)

4.7

4.8

4.5

4.4

4.9

EPS (`)

8

10

9

11

13

P/E (x)

98.0

81.5

89.3

73.9

61.3

P/BV (x)

16.9

14.3

14.1

12.5

10.3

RoE (%)

16.0

16.5

12.0

14.0

16.4

EV/Sales (x)

2.1

1.8

1.6

1.5

1.3

EV/EBITDA (x)

44.1

37.2

35.2

33.3

26.2

Source: RHP, Angel Research; Note: Valuation ratios based on pre-issue outstanding shares and at upper end of the price band

SUBSCRIBE

Issue Open: July 31, 2017

Issue Close: August 02, 2017

QIBs 75% of issue

Non-Institutional 15% of issue

Retail 10% of issue

Promoters 65%

Others 35%

Post Issu e Shareholdin g Pattern

Post Eq. Paid up Capital: `73.1cr

Issue size (amount): *`774.5cr -

**779.6 cr

Price Band: `805-815

Lot Size: 18 shares and in multiple

thereafter

Post-issue implied mkt. cap: *`5889cr -

**`5962cr

Promoters holding Pre-Issue: 76.9%

Promoters holding Post-Issue: 65.2%

*Calculated on lower price band

** Calculated on upper price band

Book Bu ildin g

Fresh issue: `362.3 cr

Present Eq. Paid up Capital: `68.7 cr

Offer for Sale: **0.51cr Shares

Abhishek Lodhiya

+022 39357600, Extn: 6811

Abhishek.lodhiya@angelbroking.com

Security and Intelligence Services (Ind.) Ltd.

IPO Note | Security Services

July 29, 2017

2

SIS | IPO Note

July 29, 2017

2

Company background

Incorporated in 1985, Security and Intelligence Services (India) Limited provides

private security and facility management services in India and Australia. They offer

cash logistics & security services, including manned guarding and electronic

security; and facility management services, such as mechanized cleaning, and pest

& termite control services.

Security services: SIS is the second largest security services provider in India, in

terms of revenue, as of March 31, 2016, and the fastest growing security services

provider in India, based on revenues for FY2010-14, according to Frost & Sullivan.

In addition, Freedonia ranks SIS’s wholly-owned Subsidiary, MSS Security Pty

Limited (“MSS”) as the largest security services provider in Australia, jointly with a

competitor, in terms of revenues, as of March 31, 2015. SIS provides a

comprehensive range of security services ranging from providing trained security

personnel for general guarding to specialized security roles in India and Australia.

In Australia, company also provides paramedic and allied health, fire rescue

services, mobile patrol, loss prevention and other related services.

Cash logistics services: SIS is the second largest cash logistics service provider in

India, in terms of market share by revenue, number of employees, ATMs served

and cash vans utilized, as of March 31, 2015, according to Frost & Sullivan. SIS’s

cash logistics business in India includes services such as cash in transit including

transportation of bank notes and other valuables, doorstep banking as well as

cash processing, ATM related services including ATM replenishment, first line

maintenance and safekeeping, and vault related services for bullion and cash.

Electronic security services and home alarm monitoring and response services: In

India, the company provides electronic security services, including integrated and

turnkey electronic security and surveillance solutions combining electronic security

with trained manpower and it has recently entered into a joint venture in order to

provide home alarm monitoring and response services.

Facility management services: SIS’s facility management services in India includes

cleaning, janitorial services, disaster restoration and clean-up of damage, as well

as facility operation and management such as deployment of receptionists, lift

operators, electricians and plumbers, and also pest and termite control. Effective

August 1, 2016, SIS acquired 78.72% of the outstanding equity shares of Dusters

Total Solutions Services Private Limited (“Dusters”), with the agreement to increase

the shareholding to 100% over the next three years. Dusters is the fourth largest

facility management services provider in India, in terms of revenues, as of March

31, 2016, according to Frost & Sullivan. Company has developed its portfolio of

services in order to cater to the needs of diverse consumer segments, including,

business entities, Government organizations and households, and to leverage the

growth and potential of such customer segments in India.

As of April 30, 2017, SIS had a widespread branch network consisting of 251

branches in 124 cities in India, which covers 630 districts. Company employed

148,678 personnel in India and rendered security and facility management

services at 11,869 customer premises across India. In Australia, company operates

in each of the eight states and employed 5,754 personnel, servicing 245

customers, as of April 30, 2017. SIS’s widespread branch network enables it to

3

SIS | IPO Note

July 29, 2017

3

service a large number of customer premises and render customized services

across India and Australia.

SIS has set up an extensive employee platform which spans recruitment,

customized training & development, deployment, incentivization and management

of personnel. Company has deep geographical reach for manpower sourcing and

training and currently operates 18 training academies across India and four

training academies across Australia. In India, company’s security services

personnel undergo extensive physical and classroom training. SIS’s personnel

recruitment, training and deployment initiatives are process oriented and

technology driven with detailed performance indicator tracking, reporting and

evaluation of personnel. SIS benefits from a pipeline of operational managers

from the graduate trainee officer program undertaken at its training academy at

Garhwa, Jharkhand, which is focused on developing a management cadre with in-

depth knowledge of company’s business and operations. SIS’s security personnel

in Australia hold required state security licenses and undergo both company-

specific and site-specific training.

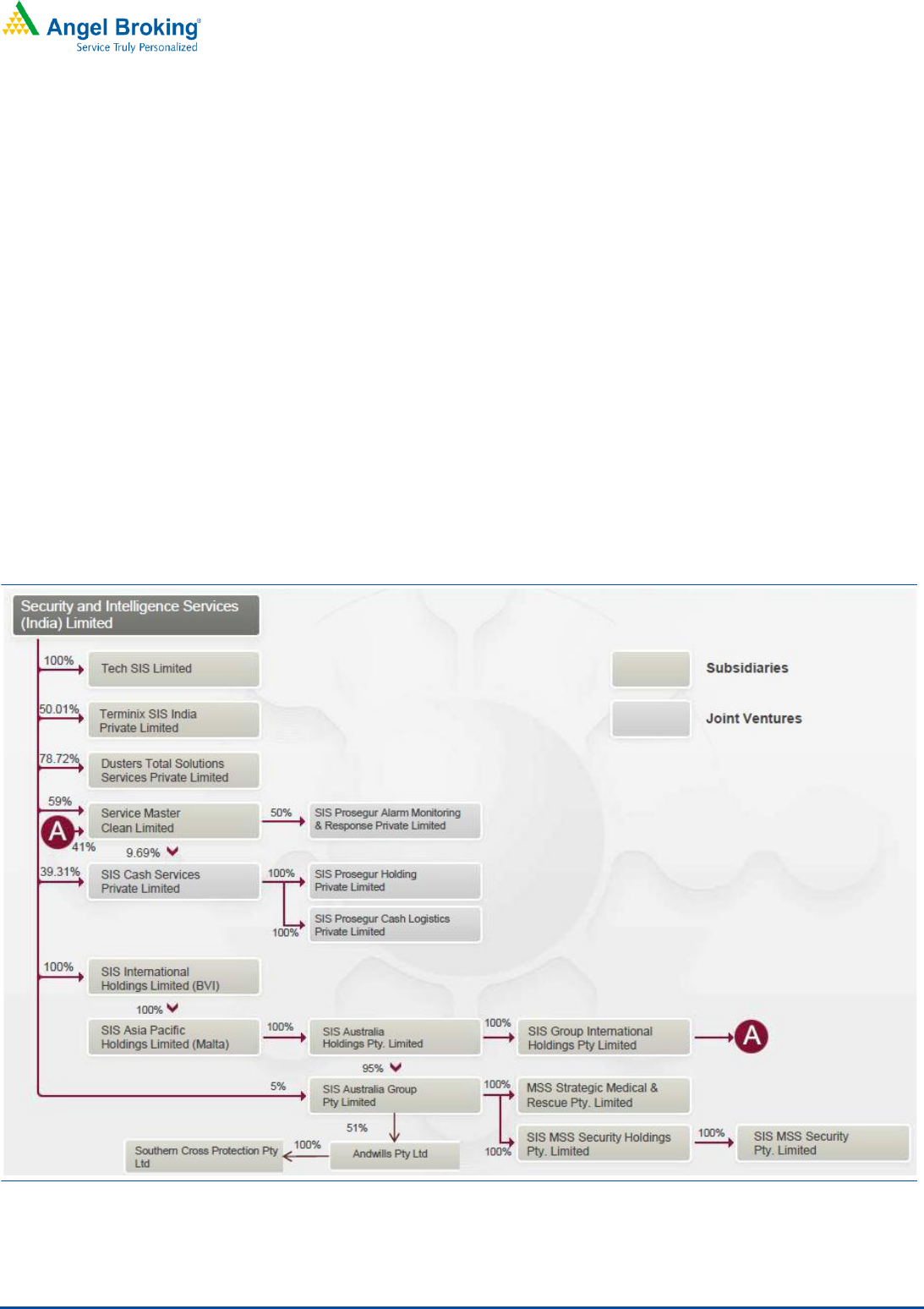

Exhibit 1: SIS Corporate Structure

Source: IPO Presentation, Angel Research

4

SIS | IPO Note

July 29, 2017

4

Issue details

The company is raising `362.3cr through a fresh issue of equity shares in the price

band of `805-815. The fresh issue will constitute ~6% of the post-issue paid-up

equity share capital of the company, assuming the issue is subscribed at the upper

end of the price band. The company is offering 0.51cr shares that are being sold

by the promoter group.

Exhibit 2: Pre and Post-IPO shareholding pattern

No. of shares (Pre-issue)

(%)

No. of shares (Post-issue)

(%)

Promoters

5,28,42,867

76.9

4,77,22,248

65.2

Others

1,58,71,383

23.1

2,54,36,787

34.8

6,87,14,250

100.0

7,31,59,035

100.0

Source: RHP, Angel Research; Note: Calculated on upper price band

Objects of the offer

Repayment/pre-payment, in full or part, of certain borrowings availed by

Company (`200cr will be utilized)

Funding working capital requirements of the Company (`60cr will be utilized)

Remaining will be utilized for general corporate purpose

5

SIS | IPO Note

July 29, 2017

5

Investment Rationale

Leadership position in all the segments

SIS is the second largest security services provider in India, in terms of revenue as

of March 31, 2016, and the fastest growing security services provider in India,

based on revenues for FY2010-14, according to Frost & Sullivan. Between

FY2013-17, company’s revenue from security services business in India grew at a

CAGR of 29.7%.

Freedonia has ranked SIS’s wholly-owned Subsidiary, MSS, as the largest security

services provider in Australia, jointly with a competitor, in terms of revenues, as of

March 31, 2015. Between FY2013-17, company’s revenue from security services

business in Australia grew at a CAGR of 7.7% in Australian Dollar terms.

SIS acquired the cash and valuables services division of ISS SDB Security Services

Private Limited (“ISS”), in December 2014 and operates it under the ‘SISCO’

brand. SIS is second largest cash logistics service provider in India, as of March

31, 2015, in terms of market share by revenue, number of employees, ATMs

served and cash vans utilized, according to Frost & Sullivan. For cash logistics

business, company has entered into a joint venture with an affiliate of Prosegur, a

global player in cash management services. SIS has established a nation-wide

network in India, comprising 80 branches, including shared branches, 2,748 cash

routes, served by 2,518 cash vans as well as two wheeler vehicles and 59 vaults

and strong rooms, as of April 30, 2017, and has set up a secure cash processing

unit at New Delhi, to service customers needs.

In March 2008, SIS entered into an exclusive license agreement with ServiceMaster

for the ‘ServiceMaster Clean’ brand, and associated proprietary processes,

operating materials and knowhow in order to develop facility management

business in India. Effective August 1, 2016, SIS acquired Dusters, the fourth largest

facility management service provider in India, in terms of revenues, as of March

31, 2016, according to Frost & Sullivan. SIS has also entered into a JV with

Terminix, a multinational provider of termite and pest control services. Company

believes that factors such as diverse range of services, customer base comprising

business entities, Government organizations and households - ranging from malls

and retail centers, hotels and hospitals to government offices and airports, and

strength of the established brands used, enable SIS to further strengthen its

leadership position.

SIS’s long-standing presence in India and Australia has enabled it to gain an

understanding of the respective markets, which the company believes has

contributed towards its operational success. SIS’s brands are well-recognized for

providing quality services in India and Australia and management believes that

strong brand positioning and strategic focus on such business has contributed to

sustained increase in business over the years.

Diverse customer base

SIS provides private security and facility management services to several customer

segments such as business entities, Government organizations and households.

These customer segments range across a variety of industries and sectors, which

include banking and financial services, IT/ ITeS & telecom, automobile, steel &

6

SIS | IPO Note

July 29, 2017

6

heavy industries, governmental undertakings, hospitality & real estate, utilities,

educational institutions, healthcare, consumer goods, engineering & construction,

which reduces vulnerabilities to economic cycles and dependence on any particular

set of customers. Company believes its ability to offer customized private security

and facility management services to fit the needs of the customers across various

business segments allows to deepen its relationships with customers and enables to

target a greater share of their requirements. SIS believes that it has been able to

retain existing customers and attract new customers because of brand visibility,

strong market position and delivery of quality services.

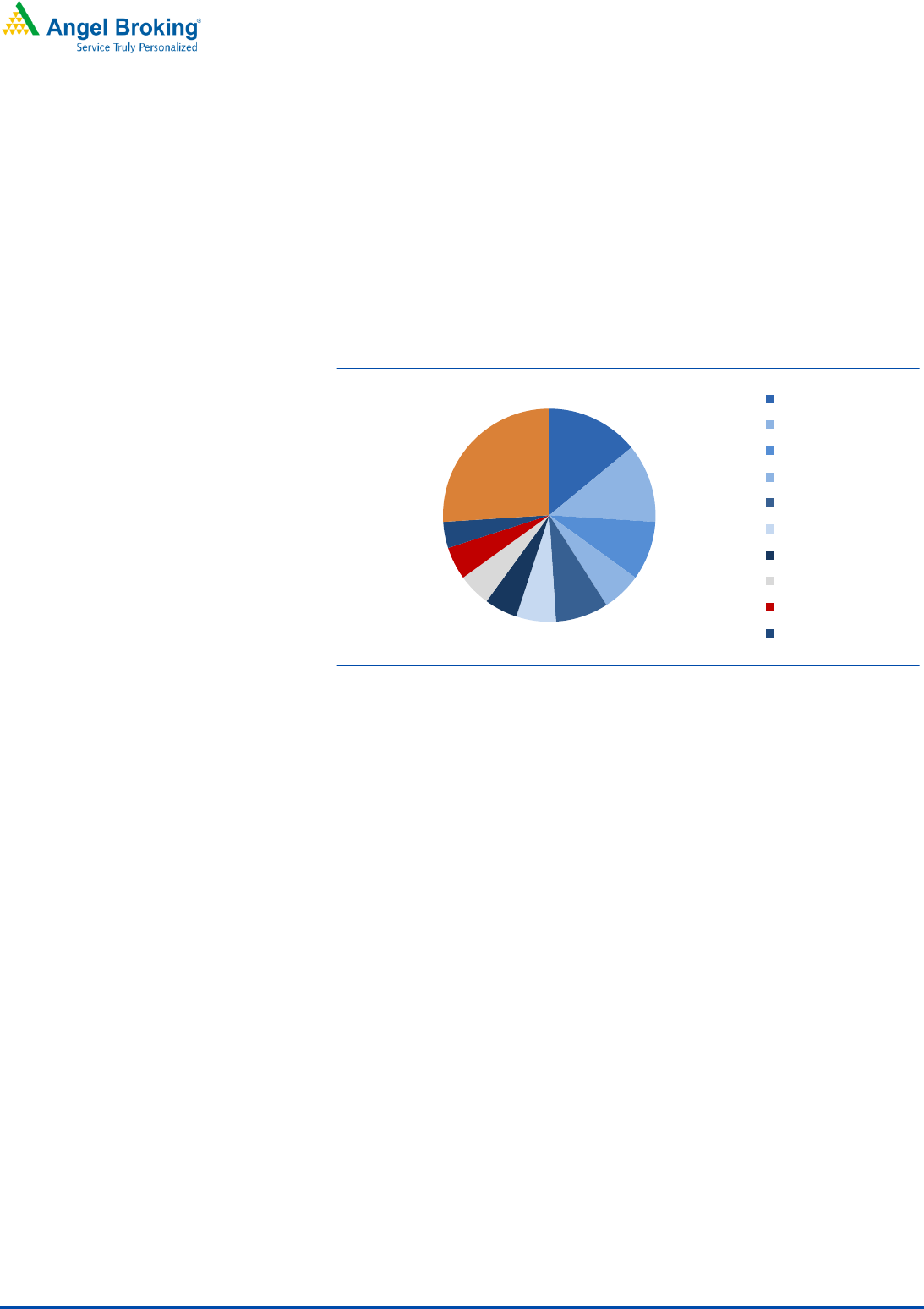

Exhibit 3: No Sector Contributes>15% of Revenues

Source: IPO Presentation, Angel Research

Diverse portfolio of private security and facility management services

SIS’s diverse portfolio of services comprises of security services, cash logistics

services and electronic security & home alarm monitoring and response, as well as

facility management services. Its security services range from providing trained

security personnel for general guarding to specialized security roles in India and

Australia. In Australia, company also provides paramedic and allied health, fire

rescue services, mobile patrol, loss prevention and other related services. SIS’s

cash logistics business includes services such as cash in transit including

transportation of bank notes and other valuables, doorstep banking as well as

cash processing, ATM related services including ATM replenishment and first line

maintenance and safekeeping, and vault related services for bullion and cash. In

India, company also provides electronic security services, including offering

integrated solutions combining electronic security with trained manpower, and has

recently entered into a joint venture to provide home alarm monitoring and

response services. SIS’s facility management services include cleaning, janitorial

services, disaster restoration and clean-up of damage, as well as deployment of

receptionists, lift operators, electricians and plumbers and pest and termite control

services.

SIS believes company’s extensive portfolio of services enables it to grow its

customer relationships and scope of engagements and serve as a single point of

contact for multiple services, driving high customer retention. Company’s multiple

14%

12%

9%

6%

8%

6%

5%

5%

5%

4%

26%

BFSI

IT/ITES/Telecom

Automobile

Steel,Heavy industries

Government

Hospitality & RE

Utilities

Education

Healthcare

FMCG

7

SIS | IPO Note

July 29, 2017

7

service offerings allow to derive operational efficiencies, by centralizing certain key

functions such as finance and sales and also certain other administrative functions.

Inorganic growth through strategic acquisitions

While continuing to maintain organic growth momentum, SIS intends to explore

inorganic expansion as well, leveraging on the experience company has gained

through its previous acquisitions.

SIS acquired 78.72% equity in Dusters Total Solutions Services Private Limited with

effect from August 1, 2016, with an agreement to increase its shareholding to

100% over the next three years. SIS acquired Dusters for a cash consideration of

`116.9cr. Effective July 1, 2017, SIS, through its 100% subsidiary, SIS Australia

Group Pty Ltd., acquired 51% equity in Andwills Pty Limited, the ultimate holding

company of Southern Cross Protection Pty Ltd., one of our current Associates, in

which 10% of the equity share capital and voting rights are directly held by SIS

Australia Group for a cash consideration of `88.4cr (AUD 17.79 Million). This

acquisition resulted in the Company, indirectly and directly, controlling 51% of the

equity share capital and voting rights in SXP.

Frost & Sullivan anticipates competition in the industry will become stiff, leading to

further consolidation of the market. Leveraging on this consolidation, SIS intends to

evaluate growth opportunities to inorganically grow operationally, including by

acquisition of cash accretive contracts from competitors, similar to the acquisition

of specified business contracts, vendor contracts, licensed properties, employees

and related assets from Scientific Security in December 2016. SIS will also continue

to consider opportunities for inorganic growth in India and the Asia Pacific region,

particularly to consolidate the company’s market position in existing business lines;

achieve operating leverage in key markets by unlocking potential efficiency and

synergy benefits; strengthen and expand service portfolio; enhance depth of

experience, knowledge-base and know-how; and increase branch network,

customers and geographical reach.

8

SIS | IPO Note

July 29, 2017

8

Outlook and Valuation

At the upper price band of `815, issue is offered at 61x FY2017EPS (Pre issue

marketcap), which is at ~36% discount to the Quess Corp (96x FY2017EPS).

Moreover, SIS has better ROE (16.4%) compared to Quess Corp (13.6%).

Furthermore, at 10.3xP/BV, 26.2xEV/EBITDA SIS’s valuation looks attractive

compared to Quess Corp’s valuation of 13.1xP/BV, 50.4xEV/EBITDA. Hence, we

recommend SUBSCRIBE rating on the issue.

Key risks

SIS is subject to several labour legislations and regulations governing welfare,

benefits and training of the employees. Any increase in wage and training

costs or if any decisions in pending cases are against the company, it could

adversely affect the business, financial condition and cash flows.

SIS is subject to risks associated with operating with joint venture and other

strategic partners.

SIS derives a significant portion of total revenue from security services

business. Any decrease in the demand for security services may have an

adverse impact on business, financial condition and result of operations.

9

SIS | IPO Note

July 29, 2017

9

Consolidated Income Statement

Z

Y/E March (` cr)

FY2013

FY2014

FY2015

FY2016

FY2017

Total operating income

2,644

3,098

3,551

3,836

4,567

% chg

-

17.2

14.6

8.0

19.1

Total Expenditure

2,519

2,950

3,391

3,667

4,345

Operating Expenses

3

3

12

11

16

Employee

2,159

2,538

2,892

3,116

3,789

Others Expenses

357

408

487

540

540

EBITDA

124

148

159

169

222

% chg

-

18.8

7.8

6.4

30.8

(% of Net Sales)

4.7

4.8

4.5

4.4

4.9

Depreciation& Amortisation

26

31

45

43

46

EBIT

99

117

114

126.3

176.0

% chg

-

18.6

(2.9)

10.9

39.4

(% of Net Sales)

3.7

3.8

3.2

3.3

3.9

Interest & other Charges

31

26

48

48

75

Other Income

14

10

15

14

10

(% of PBT)

17.1

9.9

18.0

15.0

9.0

Recurring PBT

82

102

81

93

111

% chg

-

24.2

(20.7)

14.9

20.0

Tax

29

37

33

30

22

PAT (reported)

53

65

48

63

89

Share in profit of Associates

1

1

1

11

2

Less: Minority interest (MI)

(3)

(3)

(14)

(2)

(1)

PAT after MI (reported)

57

69

63

76

91

% chg

-

22.6

(27.1)

11.9

67.0

(% of Net Sales)

2.0

2.1

1.3

1.4

1.9

Basic & Fully Diluted EPS (Rs)

8.3

10.0

9.1

11.0

13.3

% chg

-

20.1

(8.7)

20.8

20.5

Source: RHP, Angel Research

10

SIS | IPO Note

July 29, 2017

10

Consolidated Balance Sheet

Y/E March (` cr)

FY2013

FY2014

FY2015

FY2016

FY2017

SOURCES OF FUNDS

Equity Share Capital

21

6

6

6

69

Reserves& Surplus

311

386

391

443

474

Shareholders Funds

332

392

397

449

543

Minority Interest

39

36

76

3

15

Total Loans

157

200

395

400

685

Deferred Tax Liability

-

-

-

-

-

Total Liabilities

528

628

869

852

1,243

APPLICATION OF FUNDS

Gross Block

155

202

259

278

340

Less: Acc. Depreciation

57

78

136

145

180

Net Block

98

123

123

133

160

Other Intangible assets

133

128

205

175

278

Capital Work-in-Progress

6

8

7

0

4

Investments

11

11

10

12

20

Current Assets

759

837

1,065

1,092

1,524

Inventories

4

5

7

1

4

Sundry Debtors

299

253

312

288

462

Cash

253

297

374

349

451

Loans & Advances

52

31

56

68

92

Other Assets

151

250

317

387

516

Current liabilities

509

518

583

608

805

Net Current Assets

250

319

482

484

719

Deferred Tax Asset

29

38

40

47

63

Total Assets

528

628

869

852

1,243

Source: RHP, Angel Research

11

SIS | IPO Note

July 29, 2017

11

Consolidated Cash Flow Statement

Y/E March (` cr)

FY2013

FY2014

FY2015

FY2016

FY2017

Profit before tax

83

102

82

94

113

Depreciation

26

31

45

43

46

Change in Working Capital

(19)

(34)

(52)

(74)

(75)

Interest / Dividend (Net)

29

24

46

46

72

Direct taxes paid

(51)

(48)

(57)

(58)

(81)

Others

(4)

6

8

23

20

Cash Flow from Operations

64

80

71

73

94

(Inc.)/ Dec. in Fixed Assets

(43)

(54)

(47)

(66)

(67)

(Inc.)/ Dec. in Investments

16

12

(63)

14

(139)

Cash Flow from Investing

(27)

(42)

(110)

(52)

(206)

Issue of Equity

0

16

0

0

0

Inc./(Dec.) in loans

(11)

(35)

156

(18)

173

Others

(66)

26

(4)

(45)

49

Cash Flow from Financing

(77)

7

152

(64)

222

Inc./(Dec.) in Cash

(40)

45

113

(42)

110

Opening Cash balances

284

253

297

374

349

Adjustment

9

(1)

(36)

17

(9)

Closing Cash balances

253

297

374

349

451

Source: RHP, Angel Research

Key Ratios

Y/E March

FY2013

FY2014

FY2015

FY2016

FY2017

Valuation Ratio (x)

P/E (on FDEPS)

98.0

81.5

89.3

73.9

61.3

P/BV

16.9

14.3

14.1

12.5

10.3

Dividend yield (%)

0.0

0.0

0.0

0.0

0.0

EV/Sales

2.1

1.8

1.6

1.5

1.3

EV/EBITDA

44.1

37.2

35.2

33.3

26.2

EV / Total Assets

10.4

8.7

6.5

6.6

4.7

Per Share Data (`)

EPS (Basic)

8.3

10.0

9.1

11.0

13.3

Cash EPS

11.5

13.9

13.5

15.5

19.6

Book Value

48.3

57.0

57.8

65.4

79.0

Returns (%)

ROCE

20.2

19.8

14.4

14.9

14.3

Angel ROIC (Pre-tax)

44.1

41.4

28.0

25.9

23.2

ROE

16.0

16.5

12.0

14.0

16.4

Turnover ratios (x)

Asset Turnover (Gross Block)

17.0

15.4

13.7

13.8

13.4

Inventory / Sales (days)

1

1

1

0

0

Receivables (days)

41

30

32

27

37

Payables (days)

2

2

2

2

2

Working capital cycle (ex-cash) (days)

40

29

31

26

35

Note: Valuation ratios based on pre-issue outstanding shares and at upper end of the price band

12

SIS | IPO Note

July 29, 2017

12

Research Team Tel: 022 - 39357800 E-mail: research@angelbroking.com Website: www.angelbroking.com

DISCLAIMER

Angel Broking Private Limited (hereinafter referred to as “Angel”) is a registered Member of National Stock Exchange of India Limited,

Bombay Stock Exchange Limited and Metropolitan Stock Exchange Limited. It is also registered as a Depository Participant with CDSL

and Portfolio Manager with SEBI. It also has registration with AMFI as a Mutual Fund Distributor. Angel Broking Private Limited is a

registered entity with SEBI for Research Analyst in terms of SEBI (Research Analyst) Regulations, 2014 vide registration number

INH000000164. Angel or its associates has not been debarred/ suspended by SEBI or any other regulatory authority for accessing

/dealing in securities Market. Angel or its associates/analyst has not received any compensation / managed or co-managed public

offering of securities of the company covered by Analyst during the past twelve months.

This document is solely for the personal information of the recipient, and must not be singularly used as the basis of any investment

decision. Nothing in this document should be construed as investment or financial advice. Each recipient of this document should

make such investigations as they deem necessary to arrive at an independent evaluation of an investment in the securities of the

companies referred to in this document (including the merits and risks involved), and should consult their own advisors to determine

the merits and risks of such an investment.

Reports based on technical and derivative analysis center on studying charts of a stock's price movement, outstanding positions and

trading volume, as opposed to focusing on a company's fundamentals and, as such, may not match with a report on a company's

fundamentals. Investors are advised to refer the Fundamental and Technical Research Reports available on our website to evaluate the

contrary view, if any.

The information in this document has been printed on the basis of publicly available information, internal data and other reliable

sources believed to be true, but we do not represent that it is accurate or complete and it should not be relied on as such, as this

document is for general guidance only. Angel Broking Pvt. Limited or any of its affiliates/ group companies shall not be in any way

responsible for any loss or damage that may arise to any person from any inadvertent error in the information contained in this report.

Angel Broking Pvt. Limited has not independently verified all the information contained within this document. Accordingly, we cannot

testify, nor make any representation or warranty, express or implied, to the accuracy, contents or data contained within this document.

While Angel Broking Pvt. Limited endeavors to update on a reasonable basis the information discussed in this material, there may be

regulatory, compliance, or other reasons that prevent us from doing so.

This document is being supplied to you solely for your information, and its contents, information or data may not be reproduced,

redistributed or passed on, directly or indirectly.

Neither Angel Broking Pvt. Limited, nor its directors, employees or affiliates shall be liable for any loss or damage that may arise from

or in connection with the use of this information.